There Is a Risk More Terrifying Than an AI Bubble

No noise. No predictions. Just structured thinking on equity investing.

The obsession with calling bubbles is universal.

Personally, I don’t care if it’s a bubble. And if you’re a long-term investor like me, you shouldn’t either.

In fact, even if you’re a shorter-term investor, you probably shouldn’t either.

Being disinvested is probably the worst solution, and the Dot-Com Bubble is the perfect example.

The Biggest Risk Isn’t Being in the Bubble, It’s Being Out

In the 1990s, the Nasdaq went up 30x.

For comparison, going back to 1871, it took the S&P 500 109 years to achieve a similar 30x performance, which it only reached in 1980.

There is no doubt that this decade was a bubble.

Yet looking back, I’d still tell you that you should have been invested during the Dot-Com Bubble, at least up until 1998.

If you had bought before 1999, you would still be up around 48% at the bottom in 2003:

As you can see, the only years where investing would really have cost you performance were 1999 and 2000, when the bubble finally exploded in March 2000.

The Real Blind Spot in the Bubble Narrative: Opportunity Cost.

The cost of a deep crash is easy to recognize.

The cost of missing a 10x move because the entry didn’t feel “perfect” is harder to see, but just as real.

That’s opportunity cost.

To paraphrase Peter Lynch: more money has been lost waiting for bubbles than in the bubbles themselves.

I’m not saying you should be fully invested if you think we’re in a bubble.

I’m saying you shouldn’t be fully disinvested just because you think we’re in a bubble.

What matters is not whether we’re in a bubble, but when it will actually burst. And in those kinds of irrational phases, nobody can predict the timing.

Alan Greenspan was already talking about “irrational exuberance” in 1996, yet the market went on to rise for more than three years before the Dot-Com Bubble finally exploded in 2000.

The point is not to avoid pain at all costs, because you literally can’t.

You Can’t Avoid Pain, Even “God” Can’t

Charlie Munger’s words carry more weight than mine:

“If you can’t react with equanimity to a 50% market decline a few times a century, you’re not fit to be a shareholder, and you deserve the mediocre returns you’ll get.”

And history proves him right.

Imagine you could see the future and know the performance of the S&P 500 companies over the next five years:

You go long the best performers.

You short the worst.

Every five years, you update your portfolio with perfect hindsight.

You’d still experience 50% drawdowns along the way, despite superhuman performance. (Here’s my deep-dive on the study.)

So we shouldn’t care if this is a bubble. We shouldn’t care either if we’re near the bursting and the drawdown that follows, because we can’t anticipate it and we can’t avoid pain in investing.

But still… We’re not actually going to buy near or at all-time highs, are we?

Don’t ask me. Ask History.

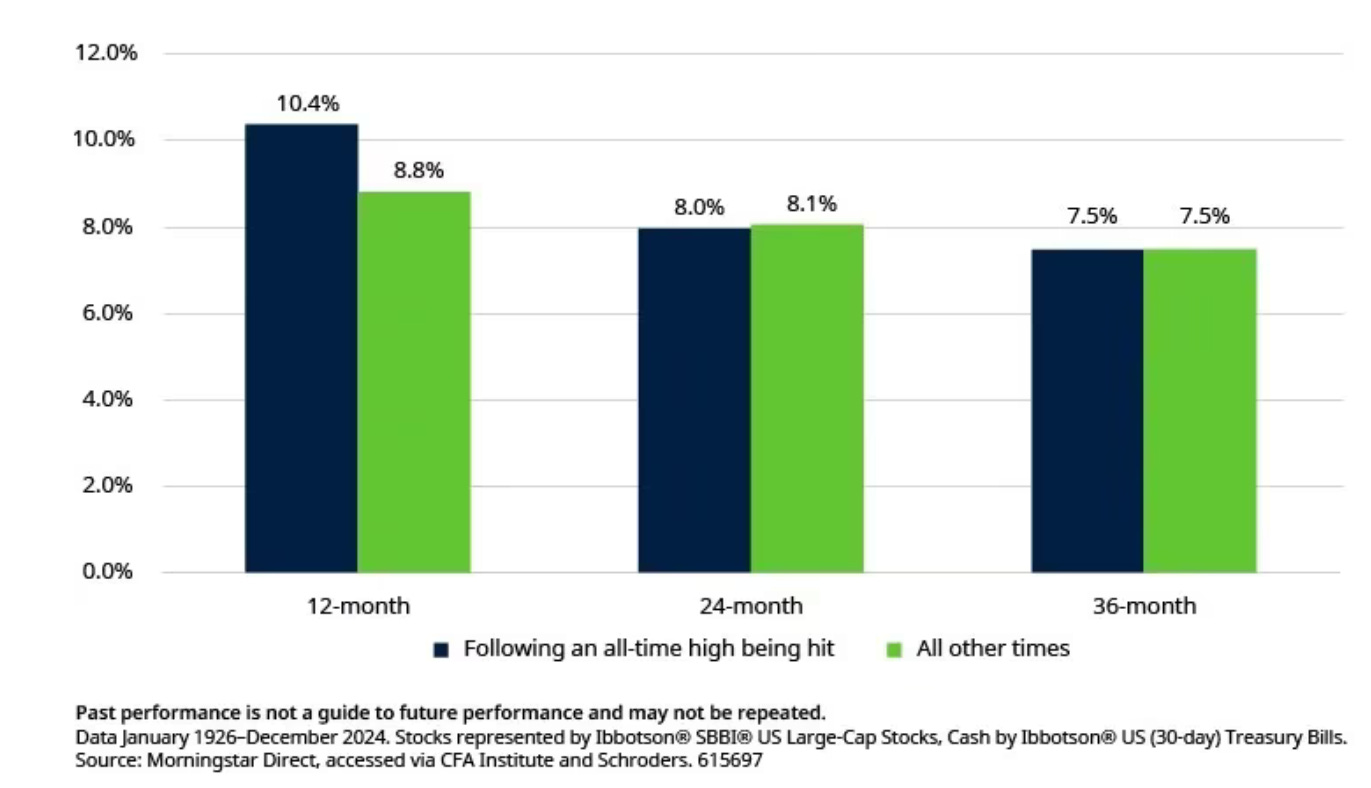

All-Time Highs Feel Dangerous. History Says Otherwise

Over the past 100 years, the performance from investing at all-time highs versus at any other time has been very similar:

Investing at ATHs has delivered roughly the same returns as investing on any random day. Over shorter horizons, it has even tended to do slightly better.

Of course, not all ATHs are the same. Bubble highs are the most painful ones, but they are also the rarest.

Over the last 100 years, the U.S. market has been at an ATH about 31% of the time (363 out of 1,187 months). Yet fewer than ten of those ATHs were followed by a deep drawdown.

In other words, if your fear of buying at the high is what’s holding you back, that fear is badly calibrated according to History.

Beyond Fear: Reduce Uncertainty

Our biggest job as investors is to manage opportunity cost.

The whole point of this post is to show that being fully disinvested probably has a huge opportunity cost, because:

Even if it’s a bubble, the market can stay irrational for years.

The fear of drawdowns is useless, because you can’t avoid them.

The fear of buying at ATHs is irrational, because the market is at an ATH about one-third of the time and delivers similar returns to any other entry point.

But “not being disinvested” doesn’t mean being invested without a plan.

Not understanding your companies and not knowing what you’ll do with them, can be far more costly than the opportunity cost you’re trying to avoid.

Knowing your companies and having a plan reduces uncertainty and minimizes behaviors that destroy compounding, like panicking during drawdowns.

Know your companies. Know your plan. Expect pain. Compound.

That’s all it is.

Half way through, wanted to say this is a great perspective.

Your writing is excellent, and everything you say is well-grounded