IQ < RQ in Investing

I could even have written “RQ > IQ in Life”, but it would just be an opinion.

TL;DR

Intellectual Quotient (IQ) = ability to compute; Rationality Quotient (RQ) = ability to make robust decisions under uncertainty.

RQ = quality of beliefs (epistemic rationality) + ability to turn those beliefs into robust decisions (instrumental rationality).

The greatest investors have a high RQ, not necessarily a high IQ. Their RQ is what allows them to survive long enough to compound for decades.

RQ can be trained and developed continuously. It’s a daily, lifelong battle.

A complete method to train your RQ is provided at the end of the post. The core idea is to build a repeatable process that generates feedback, and to use that data to improve.

The edge comes from your ability to repeat these long, boring steps over time. Simple, but not easy.

Here’s the sad reality: if your IQ is 130, you won’t train your way to an IQ of 170.

Fortunately, as an investor, having a high IQ isn’t necessary. In fact, it can sometimes even hurt performance.

There’s another “quotient” that matters far more.

Even better, it’s something you can actually train.

So let’s dive into this powerful concept: the rationality quotient.

IQ vs RQ

Imagine it’s 1972. You invest $1 million in the Nifty Fifty, a group of 50 U.S. companies considered “blue-chip” darlings and wildly popular at the time (Coca-Cola, Johnson & Johnson, McDonald’s, etc.).

You put $20,000 into each company. You take a (very) long nap, wake up in 2025, and discover that 49 of the 50 companies went to zero. Yet you’re happy. Why?

Because the one company that didn’t go to zero is Walmart. Up 13,736x over 53 years (a 19.7% CAGR), your $20,000 turned into $274.72 million.

If you had invested your $1 million in the S&P 500, you would have ended up with only $68.6 million (excluding dividends in both cases).

Now imagine that, before you invest and take your (very) long nap, someone walks up to you and says: “Careful, 49 of these companies are going to go bankrupt.” What do you do?

Build complex models? Analyze each company in depth, grinding through decades of data? Use the computational power your high IQ makes possible?

Or instead, use your rationality, and ask the following questions:

How much do I stand to make if I buy them all versus investing in a smaller number and hoping I include the winner?

How much do I stand to lose if I pick only a few and miss the winner?

How long will this research take, and what range of outcomes could it realistically change?

Here, your rationality is far more useful than your intelligence. As Warren Buffett put it1:

“How I got here is pretty simple in my case. It’s not IQ, I’m sure you’ll be glad to hear. The big thing is rationality. I always look at IQ and talent as representing the horsepower of the motor, but that the output—the efficiency with which that motor works—depends on rationality.

A lot of people start out with 400-horsepower motors but only get a hundred horsepower of output. It’s way better to have a 200-horsepower motor and get it all into output.”

What RQ Really Is (and Why It Beats IQ)

Put simply, the rationality quotient is your ability to make high-quality decisions in an environment of uncertainty. Conveniently, that’s exactly what investing is, at its core.

Rationality has two main components.

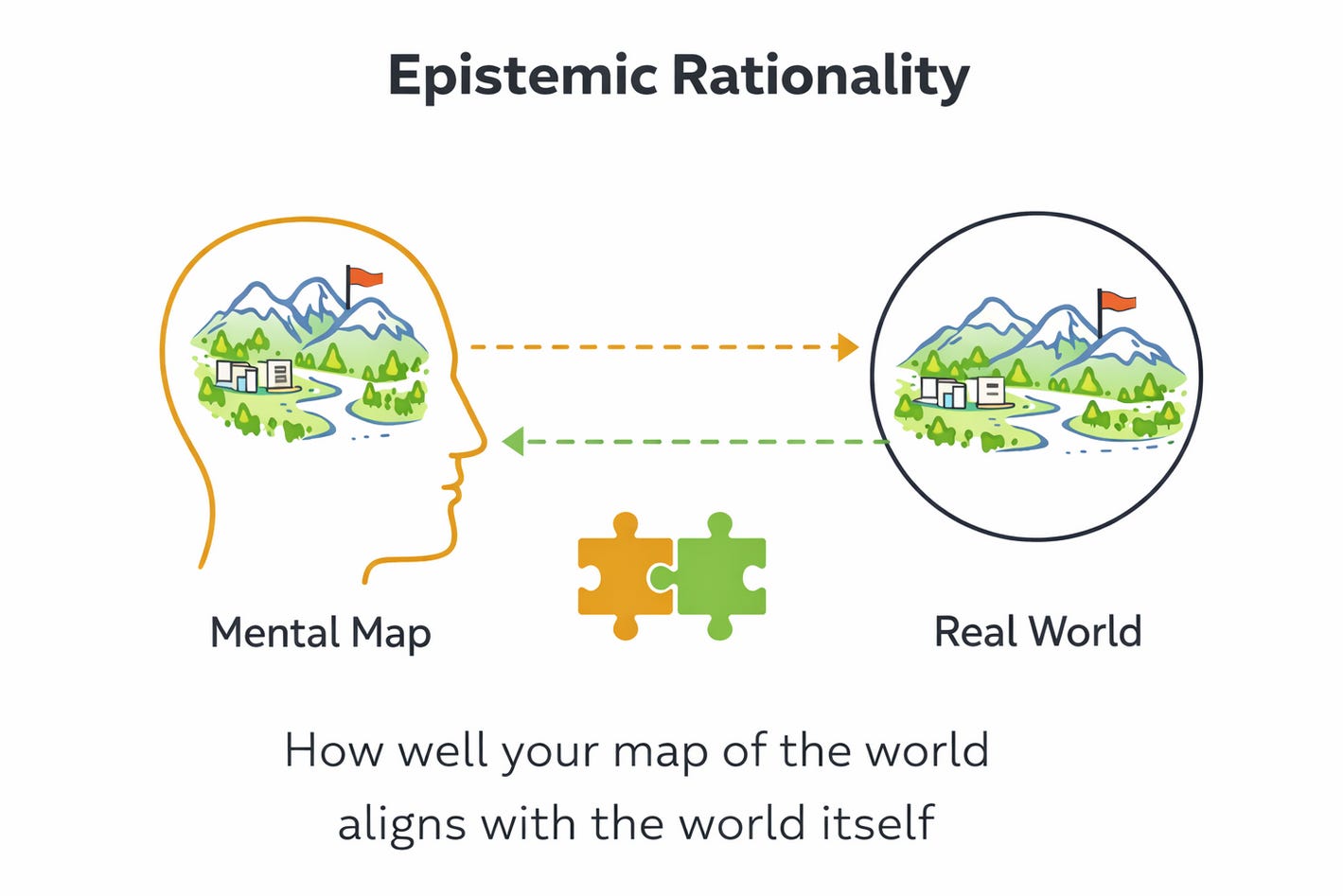

Epistemic Rationality

As cognitively limited humans, we navigate the world through biased perceptions, from which we infer beliefs. For example: I don’t feel any movement when I’m standing still, so the Earth must not be moving.

A rational person, however, knows that this belief could be wrong, so they attach a probability to it.

Epistemic rationality is the quality of those beliefs. In other words: how well your beliefs, and the probabilities you assign to them, match reality.

A more visual way to put it: it’s the alignment between someone’s mental map of the world and the world itself.

Instrumental Rationality

Instrumental rationality begins once you have a belief. It’s your ability to take that belief and execute an action under constraints: constraints of time, capital, knowledge, and so on.

Concretely, instrumental rationality can be broken down into five steps:

Clarify the objective → Define precisely what you’re trying to achieve.

Identify the options → What you can do, at what cost, with what probability of success, etc.

Evaluate the consequences → What it costs, what it could deliver, and the probabilities attached to each outcome.

Choose → Amid all this uncertainty, select the action with the best trade-off between expected results, risks, and costs.

Revise → Notice when constraints or information have changed, then repeat the first four steps.

Applying this to Investing

For an investor, epistemic rationality is the art of turning an intuition into a structure: “here is my base case, here are the alternatives, and here are their relative probabilities.”

What matters isn’t finding the “true” probability (it doesn’t exist). What matters is having a coherent system that forces you to make your uncertainty explicit, and to measure it.

The hard part is that this isn’t a one-off exercise. It’s a living process. With every new piece of information, you have to answer: “does this increase or decrease the probability of my scenario, and why?”

But updating probabilities is only half the job. The other half, instrumental rationality, is acting: turning those imperfect beliefs into robust decisions.

In an uncertain environment, a rational decision isn’t the one that maximizes gains in the best-case scenario. It’s the one whose results stay acceptable across a wide range of scenarios.

This is where Buffett’s quote really matters:

"Rule No. 1: Never lose money. Rule No. 2: Never forget Rule No. 1."

The goal is not to avoid any loss. It’s to design decisions whose downside stays limited even when you’re wrong.

Great investors don’t get their edge from precision, but from the structure of their decisions:

they make money when favorable scenarios play out,

they lose little (relatively) when they don’t.

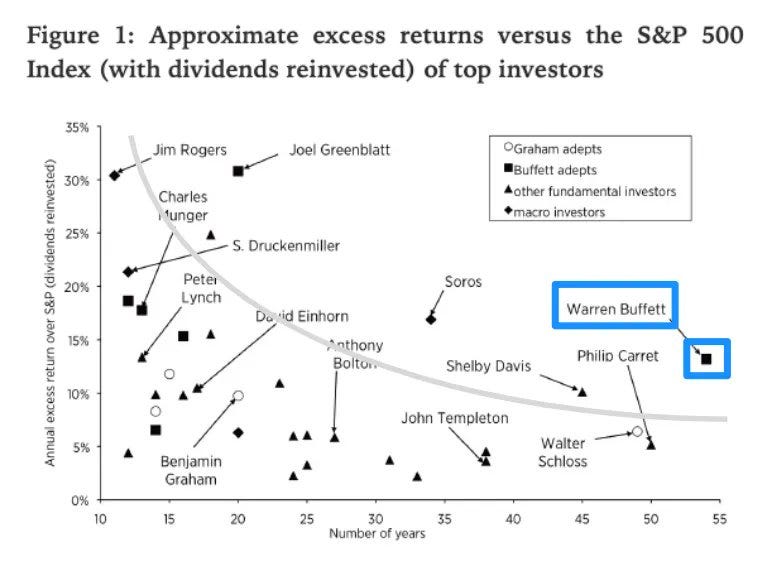

That asymmetry, and the ability to repeat it over time, is the mark of a truly great investor.2

Every name on this chart belongs to someone who focused on protecting their capital first.

The real question is: what can we do to maximize our chances of appearing on a chart like this one day?

Increase Our RQ as Investors

Here we’re talking about cognitive skills. There is no magic shortcut.

The key is to have a structured process, repeat it, and evaluate it by creating a feedback loop.

Train Epistemic Rationality

The goal here is to move from opinion to forecast:

Write our beliefs in a forecasting format.

For example: “I think that in 1 year, margins will be above the base rate in 80% of cases.”

Place each possibility within a set of scenarios.

Have at least a base case, an upside case, and a downside case, with probabilities attached.

Have explicit reasons that could make us shift from one to another.

Have a coherent, standardized system to assign probabilities.

Use a stable, comparable scale to measure uncertainty. That scale can use numbers, but also words.

Don’t fall into the trap of false precision. A range is often better than a single value. For example, saying something is likely with a 60-70% chance is better than throwing out 68.3% without any explicit reason.

Keep a log of our forecasts and reassess them later.

This is probably the most important point, because it’s what creates feedback and helps us calibrate future forecasts.

The goal isn’t to be right. It’s to be honest about our uncertainty, which is exactly where many investors fail.

Train Instrumental Rationality

Investment performance comes from compounding. The absolute priority is survival, and all of these rules should ultimately serve that.

Make the decision depend on probability.

The higher our confidence level, the more intense the action should be.

“When you have tremendous conviction on a trade, you have to go for the jugular.” - Stanley Druckenmiller

Set fixed, intrinsically robust rules.

For example, simple guardrails: concentration limits, minimum liquidity, low implicit correlation between two assets, etc.

Always be confident enough that the decision will remain acceptable, even if the adverse scenario happens.

Define an execution framework upfront, and stick to it.

In investing, the actions are buy / sell / do nothing. Everything else is an execution framework: position sizing, when to sell, when to add, etc.

The goal is to have an explicit execution framework that leaves us no room for interpretation in the heat of the moment.

The hardest part isn’t defining the framework, it’s sticking to it. And that’s exactly where we can develop an edge: by doing the complicated, boring, or “apparently useless” things consistently.

Improve the Whole Process

The rules above give us a lot of data. But real progress comes from turning that data into feedback, and then updating our system.

Review the data periodically.

Compare our forecasts to real outcomes, then analyze the gap and where it came from (missing information, wrong weighting, etc.).

Always separate good decisions/bad outcomes from bad decisions/good outcomes. Judge the bet, not the outcome.

Identify our biases.

Spot the obvious ones that consistently lower our RQ (FOMO, overconfidence, poor interpretation of information, etc.).

Start with the bias that’s simplest and most obvious to fix. For example, if FOMO is hurting our performance, implement a simple rule: always wait 24 hours before taking action.

Having a higher RQ makes us better investors:

The good news is that RQ is trainable.

The “bad” news is that the training looks like boring, slow, repetitive, and uncomfortable.

That’s actually a blessing. If it were fun and easy, everyone would do it. And markets would offer far less performance to those who do the work.

But there’s no way around it: you only get the benefit if you consistently do these boring, long, repetitive actions.

That’s precisely why investing is simple, but not easy.

The real question is: Are you willing to do hard things, over and over again?

The quote comes from an article by Mauboussin and Callahan, which I drew heavily on when writing this piece:

Mauboussin, Michael J., and Dan Callahan, CFA. IQ versus RQ: Differentiating Smarts from Decision-Making Skills. Credit Suisse Global Financial Strategies, May 12, 2015.

“There are old traders and there are bold traders, but there are no old bold traders.” Even though this quote comes from the trading world, I think it applies just as well to investing and reflects the same underlying process.

Rationality could delusive.

Without the basis of IQ, RQ collapse.

IQ is the mother of RQ.